The international scientific and analytical, reviewed, printing and electronic journal of Paata Gugushvili Institute of Economics of Ivane Javakhishvili Tbilisi State University

FINANCIAL SYSTEM STABILITY AS INTEGRAL PART OF MONETARY POLICY FRAMEWORK

DOI: 10.36172/EKONOMISTI.2020.XVI.03.LEMONJAVA.TKESHELASHVILI

Annotation

Monetary policy decisions are transmitted to the economic through financial system. Moreover, financial stability is objective of monetary policy risk management system, which allows analyzing the impact of using different transmission channels on both economic and financial environments. Monetary policy rate is the basic instrument, which has a direct influence and at the same time is one of the main risks to which the financial system is most sensitive (prices, liquidity, over indebtedness). On the one hand, in order for monetary policy to be effective, a robust financial system is needed and price stability is a prerequisite for financial system stability. Financial markets which are characterized by different shocks have direct influence on economic activity and latest financial crisis is vivid example which started from banking crisis and spread to the economy. Despite critical expert opinions, central banks nowadays agree that financial sector stability is and should be part of the monetary policy framework, however, price stability on its own does not guarantee a stable financial system, without adequate regulations and strict supervisory policies. In order to de-risk Georgian banking sector, National Bank of Georgia strives to approximate with the best international standards -fully Basel III compliant in addition to encouraging sound lending environment

Keywords: Monetary Policy, Financial System, Risk Management, Basel III

1. Financial System and Associated Risks

Nowadays, Georgian financial system consists of 15 registered Banks, 2 Non-Bank Depository Institutions, 48 Microfinance Organizations, 844 Exchange Bureaus, 2 Stock Exchanges, 17 Insurance Companies and 3 Pension Schemes. Net assets of these financial institutions amounted to USD 54 billion out of which 75 % is attributed to Banks.

Banks are at the heart of the world financial system. At present, no modern economy can exist without functioning banking system since, economy needs money, which circulates through banks. It is banks that proceed money flows between central bank and private sector, companies and their customers.

In many developed countries and especially in developing ones, where investment security markets are less developed banks role is huge since, mainly access to money resources is available from them. Respectively, in such counties without borrowings it would be impossible to finance and develop manufacturing, agriculture, tourism or any other sector of economy. Banks, on the other hand, with a wide span of consumer loans, help the private sector to acquire business-produced goods and services. With the aforementioned services of banks, many customers can purchase their own apartment, car or finance their studies. Additionally, banks process clients’ multitude purchases of goods or services via money transfers, checks, credit cards internet banking or other remote channels, daily. It is therefore logical that banks play such an important role in the modern economy. However, lending is just one side of the medal. There is also no doubt that banks have a special role in mobilizing the money needed to finance these loans. Even in low-income countries, banks via tailor-made deposit products try to attract consumers, thereby helping to create a -saving culture for future needs. At the same time, banks ensure the safekeeping of savings in the economy. Considering all of the above, role and function of the banks may be determined by the following two main characteristics:

Provider of wide range of banking products and services.

Traditional intermediary role

Banks are known for a wide range of financial services offered to government, legal entities or private individuals. Banks, which nowadays are in tough competition, do not limit themselves with traditional services like deposit attraction and disbursement of credit facilities but also offer their clients investment, consulting, insurance, risk management and many other additional services. Over the last two / three decades, banks have become universal financial service providers via constantly developing new, innovative products and offering them to their customers. Consequently, it should come as no surprise that in a number of industrialized and developing countries, including Georgia, the banking sector has emerged as the most important, growing and profitable sector of the economy.

Along with the services and products offered, as mentioned above, it is important to discuss separately the main economic function of banks: creating money via local and international payment systems; Mobilizing savings as deposits and its transformation into working capital though credit facilities. By lending to enterprises, government and private individuals, banks play intermediary role in the economy by money supply (deposits) and money demand (loans). In other words, with this unique intermediary function, banks perform deposits attraction (which are savings for future that less likely to circulate in economy) and delivering them to entities who are willing to invest in new projects or even spend for personal purposes. Not only it stimulates but in many cases, it is crucial for economic growth, job creation and increase the living standard in general.

Recently, especially in the wake of the nearest global financial crisis, the question has often been raised on whether the banks are really required to perform the above-mentioned intermediary function. Let us briefly discuss what fundamental difficulties entities may face (the difficulty of verifying the borrower's creditworthiness and trust factors are being ignored at this stage):

They may simply not agree on the loan term. As is well known in most cases, those who want to save money tend to focus on short / medium term (1-2 years on average). Borrowers, on the contrary, need amounts for relatively longer period (mortgage loans for example up to 15 years).

The following problem may be the interest rate type. For example, if interest rates are generally expected to rise in the market, the borrower prefers to invest the money in a floating interest rate (so that future interest rate hikes will have a positive impact on his income). The borrower, in this case, will certainly be interested in borrowing at a fixed rate.

Finally, may not agree on currency. For example, due to the expected depreciation of the local exchange rate, the depositary will be interested in saving in hard currency (like US dollars or Euros). A borrower who has income in local currency would certainly prefer to borrow in the same currency.

Consequently, even though it may be theoretically possible to reach a direct agreement between these entities, however, due to the above difficulties, it is unlikely to happen. The solution to these difficulties is the role of the bank as a financial intermediary in the economy. In order to fulfill this unique function, banks are making the following transformations:

Maturity Transformation: The transformation of short-term funds into relatively long-term credit facilities.

Interest Rate Type Transformation: The transformation of funds attracted into floating interest rates into fixed interest rates and / or vice versa.

Currency Transformation: The exchange of funds attracted in one currency into loans in the other currency.

It should also be noted that the economic environment is constantly changing, causing changes of various financial indicators (such as interest rates or exchange rates, etc.). Consequently, it is clear that significant financial risks arise during the abovementioned transformations, and effective management of these risks is one of the prerequisites for the successful operation of the Bank, and the existence of a stable financial system from the standpoint of the Central Banks.

The most common risk categories are: credit risk, legal risk, reputation risk, strategic risk, compliance risk, operational risk, liquidity risk, market risk. From the listed risks, liquidity and market risks (currency risk, interest rate risk) fall into the financial risks category. Below are provided definitions of these basic risks as per Decree of National Bank of Georgia:

Credit risk:

Credit risk is risk that counterparty fails its payment obligation or default. Credit risk may arise from various banking activities with its clients (hereafter debtors) and partners such as lending, treasury operations, investment activities and trade financing.

Legal risk:

Legal risk is a risk that is caused by legal weaknesses, which, among other factors, result in legal actions, lack of auxiliary provisions in laws or regulations or weakness of legally binding requirements such as non-compliance with legal requirements of contracts and others.

Reputational risk:

Reputation risk is the risk that, among other factors, results in negative public statements about the bank's operations or negative performance of the bank.

Strategic risk:

Strategic Risk, which, among other factors, leads to poor planning and poor implementation of the Bank's strategy, weak business decisions of the Bank or failure to respond to external changes.

Compliance risk:

Compliance risk is the risk of legislative and regulatory sanctions, financial losses, or the loss of a bank's reputation that could result in failure to comply with laws, regulations and standards. As a rule, with respect to laws, regulations, compliance risk is an integral part of banking risks, such as minimum capital requirement, quality of Income earning assets, loan loss provisions, macroprudencial limits, and annual budgets/strategy and other risks related to specific provisions.

Operational risk:

Operational risk is the risk of loss due to inadequate internal processes, human actions, systems and external factors. Operational risk is defined as the risk of loss resulting from inadequate or unsuccessful internal processes, personnel and systems, or external factors. Operational risk can result in direct or indirect financial losses. Operational risk can be characterized by any of the Bank's activities, such as lending, treasury, investment and operating activities, services, trade finance, credit and debt instruments, information technology and information system management, as well as human resources management.

Liquidity risk:

Liquidity risk, in the narrow sense (default risk), means the risk that the Bank will no longer be able to fully or timely fulfill its current and future payment obligations. To do this, the bank must always have sufficient liquidity to meet its obligations, even in emergencies (during stress periods).

Liquidity risk in the broad sense (risk of financing) means the risk that the bank will not be able to obtain additional financing or be able to obtain it, though at significantly increased market interest rates. Liquidity risk is the risk that the Bank will not be able to settle its liabilities within the set timeframe. Liquidity risk can be divided into the following categories:

- Market liquidity risk, in particular the risk of weak market liquidity due to the situation or market problems, the bank is unable to balance certain positions with market prices.

- Liquidity risk of financing, in particular the risk that the bank will not be able to provide cash or attract funds from other sources.

Liquidity risk may incur in a variety of ways from banking activities such as lending, treasury and investment activities, trade finance and other. Liquidity risk management is extremely important, given that liquidity problems can be devastating not only for the bank but for the banking sector as a whole.

Market risks:

The fluctuation of prices in markets affect to the performance of financial organizations. These prices may be expressed in percentage rate, exchange rate, price of goods or value of shares. Market risks may incur in a variety of ways from banking activities such as lending, treasury and investment activities, trade finance and other. For example, if an organization has assets or liabilities at a floating rate, its fluctuation will affect the profitability of the company. For organizations involved in international trade, or high dollarized balance sheet structure, it is likely that the change in the local currency exchange rate with respect to foreign exchange will have a corresponding effect.

In respect to Foreign exchange risk it refers to the adverse effects of an exchange rate change on the Bank's financial position and capital adequacy. Currency risk is the change in the Bank's local currency exchange rate against the foreign currency. It arises when there is no matching of assets and liabilities currencies “Open Currency Position”. Bank may gain a loss if has an open currency position (aggregate). In recent years, the market environment has given rise to speculative trading under naturally floating exchange rates, which in itself has increased currency risk. Currency risk arises when there is no match between assets and liabilities denominated in the same foreign currency. Given that currency risk is speculative in nature, its change may cause a profit or loss to the company. Inflationary pressures on interest rates in foreign and local currency may also lead to fluctuations in the local currency, giving rise to currency risk. Such fluctuations are often caused by macroeconomic factors and occur for a long period, although the specificity of the foreign exchange market can identify the trend in time. Other macroeconomic aspects affecting the local currency, such as the country's trade volume and direction and capital flows. Short-term factors such as expected or unexpected political events, changing expectations of market participants, or speculative currency trading may be the cause of currency fluctuations.

2. Monetary Policy

Monetary policy is the macroeconomic policy that allows central banks to influence the economy. It involves managing the money supply and interest rates to address macroeconomic challenges such as inflation, consumption, growth and liquidity.

Central banks are responsible for the creation and implementation of monetary policy, the stability of the exchange rate, and the control of monetary aggregates in the economy, ensuring price stability. For a long time, the task of monetary policy was limited to exchange rate control, which was in turn fixed at the gold standard (at the beginning of the 20th century) for the purposes of stimulating international trade. Ultimately, such policy contributed to the Great Depression of the 1930s. After the depression, governments made employment a priority. Central banks have changed their direction based on the relationship between unemployment and inflation, known as the Phillips Curve. They believed in the link between unemployment and inflation stability, so they decided to increase aggregate demand using monetary policy (money supplying to economy) and keep unemployment low. However, this was the wrong decision that led to the stagflation in the 1970s, which was further compounded by the 1973 oil embargo. Inflation rose from 5.5% to 12.2% during 1970-1979 and reached a peak of 13.3% in 1979.

In order to keep inflation under control, two monetary institutions are needed. Public and institutional readiness to make price stability a long-term goal of monetary policy (Mishkin F. S., 2004). Institutional readiness may be prescribed by law and be the central bank's goal however, support for price stability by the public and politicians is more important than determining the level of law. Numerous examples in the past have shown that even in the developing world, laws change so readily that the objective set at the level of law alone is not sufficient to achieve the desired result.

The second important factor for successful inflation targeting is the willingness of the public and the institutions of central banks to be fully independent from the outset. Independence means that central banks should be prohibited from financing state deficits, and should be able to identify and use monetary instruments without government interference (Mishkin F. S., 2004).

In recent decades, central banks have developed new management techniques, called inflation targeting, that control the growth of the overall price index. In fact, currently most leading countries use inflation targeting. New Zealand was the first county choosing inflation targeting regime in 1990, which was followed by Canada in 1991, Great Britain in 1992, Switzerland Finland and Austria in 1994. Israel, Norway, Poland, Romania, Greece, Turkey, Georgia also have adopted inflation targeting regime.

Since 2009, the National Bank of Georgia’s monetary policy regime has been inflation targeting, likewise in all developed and many developing countries. Despite the regime has been proven to be the most effective it still has its challenges. In contrary to exchange rate or monetary aggregates, inflation control is not easy. Effect from monetary policy instruments make effect (path through) on inflation only after some lags. Controlling inflation is much difficult in developing counties since, inflation has to be pushed down from high levels. In such circumstance, it is high error probability in inflation forecasts, which results in missing targets. It will be very difficult to build credibility on inflation targeting strategy and hard to explain the reasons of not meeting the targets from monetary authority perspective. It is proven effective strategy, when adoption happens gradually and it is preceded by a decline in inflation (Paul,R.M. Miguel, A.S. Sunil, Sh., 1997). High dollarization may complicate inflation targeting. In many developing countries the balance sheet of companies, households, banks is substantially dollarized, with both assets and liabilities on both sides (Guillermo, 1999). Since, floating exchange rates are required for inflation targeting, fluctuations in the exchange rate are inevitable. However, the large and sharp depreciation of local currency increases the burden of foreign currency denominated debts, which causes a massive deterioration of the balance sheet and increases the risks of financial crisis (Mishkin F. , 1999). Developing countries do not have the luxury of ignoring the exchange rate when conducting monetary policy under the inflation targeting regime, but the role should clearly serve the purposes of inflation. Inflation targeting, especially for dollarized economies, may not be effective until strict prudential regulations and appropriate oversight of financial institutions ensure the stability of the exchange rate shocks.

Price stability is the mandate of 60% of countries Central Banks. According to a survey by the Central Bank of Poland (Niedźwiedzińska, 2018), of more than 40 countries with a inflation targeting regime, 14% have the sole mandate of price stability and 86% have mixed objectives. From mixed mandates, 52% prioritize price stability and 33% do not have explicit priority. Mixed objectives include price stability, economic activity, financial stability and other goals. Price stability is also concerned with maintaining the value of money. Economic activity has a broader interpretation, but it is also concerned with promoting full employment. Financial stability includes supporting the development of the banking system, while other objectives include a stable payment system. Out of 14 inflation targeting countries with no explicit prioritized objective there are 5 developed countries (Australia, Canada, Switzerland, UK, USA) and 9 developing countries (Argentina, Brazil, Chile, Dominican Republic, Guatemala, Paraguay, Russia, Thailand, Uganda). Price stability is a priority for 22 countries (8 developed countries and 14 developing countries including Georgia). Among the six countries with the only mandate of price stability are 1 developed country New Zealand and 5 developing countries: Colombia, Kazakhstan, Peru, the Philippines and Romania. After price stability, priority is economic activity, which aims to promote sustainable and full employment. The objective of economic activity is prioritized by 30 countries (12 developed and 18 developing). Financial stability takes second place after economic activity. The financial stability mandate has 23 countries out of which 6 are developed and 17 are developing.

Also, inflation target level is important factor and according to a survey by the Central Bank of Poland (Niedźwiedzińska, 2018), the developed countries when first establishing the regime set inflation target at 3.8% on average and now the average target of 2.1%. In developing countries, the initial target was 6% on average and 4.3% in the current period.

The main objective of the National Bank of Georgia is price stability, but it also ensures the stable functioning of the financial system if possible so as not to jeopardize its primary objective. Monetary policy instruments are limited to refinancing loan, one-month open market operation, overnight deposits/loans, certificates of deposit, treasury securities and reserve requirements (liabilities in national currency 5% and liabilities in foreign currency 25%).The transmition channels include: interest rate channel, credit channel, exchange rate channel and expectation channel.

3. How does monetary policy relates to the stability of the financial system, and how can the stability of the financial system be considered within the monetary policy framework?

Monetary policy decisions are transmitted through the financial system to the economy accordingly, taking into account this intermediate function, the monetary policy framework is always taken into account in the financial system environment. Moreover, the monetary policy risk management system considers the objective of financial system stability, which allows analyzing the impact of the use of different channels on both the economic and financial environment.

Interest rate is the main instrument of monetary policy, which, has a direct impact and is also one of the main risks to which the financial system is mostly sensitive to (prices, liquidity, over indebtedness). On the one hand, in order for monetary policy to be effective, a strong financial system is needed and price stability is a prerequisite for financial system stability. The shocks on the financial markets have a direct impact on economic activity as evidenced by the recent global financial crisis that started from the banking crisis and spread to the economy, affecting aggregate demand and inflation.

Numerous analytical papers have provided answers on how monetary policy should respond to financial imbalances and how best to combine monetary policy and macro-prudential policies (Collard, F. Dallas, H., Diba, B. & Loisel, O., 2017), (Paoli, B. & Paustian, M. , 2017), (William G. Tierney & Randall F. Clemens, 2011), (Rubio, M. & Carrasco-Gallego, J. , 2016) etc. According to

Benoit Coeure (Member of the Executive Board of the ECB) monetary policy can only win from integrating banking supervision in a central bank in particular four areas in this respect: the state of the macroeconomy, monetary policy options, interactions with supervisory policies and the management of the central bank balance sheet and that these opportunities are greater in turbulent times. At least three types of challenges and risks need to be managed when integrating supervision in a central bank alongside monetary policy: potential conflicts of interest, reputational risks and central bank independence. However, there are critical expert opinions and according to them it is believed that monetary policy should be clearly segregated from the objective of financial stability, both at the level of policies and regulations and at the level of regulatory authorities. Lars Swensson (Svensson, 2017) considers that monetary policy should never aim for financial stability, monetary policy and macro-prudential policies should be governed by different bodies and should not be coordinated between them.

4.De-Risking Georgian Banking Sector

In order to de-risk Georgian banking sector, National Bank of Georgia strives to approximate with the best international standards: capital buffers, leverage ratio, liquidity coverage ratio (LCR), net stable funding ratio (NSFR) which are fully Basel III compliant also, encouraging sound lending environment via introducing payment to income (PTI) and loan to value (LTV) limits, requirement of formal proof of income, 50% cap on interest rates.

The objective of the National Bank of Georgia macro-prudential policy is to reduce financial sector procyclicity, excess lending, dollarization, excess concentration and other systemic risks. In addition, the goal of macroprudential policy is to increase the financial system's resilience to existing risks (National Bank of Georgia).

Capital requirements (buffers are expressed as a percentage of risk-weighted assets):

Capital requirements under Pillar I:

1) Core capital buffer-4.5%

2) Tier1 buffer-6%

3) Total capital-8%

Combined buffer:

4) Capital conservation buffer-this buffer constitutes 2.5% of risk-weighted assets and it is necessary to comply during ordinary business cycle. If the buffer falls below the threshold during stressful environment, banks should ensure to eliminate by reducing the distribution of income for example: No dividend or bonus payout is allowed until the buffer reaches its mandatory level. The conservation buffer is an extra pillow that can be used in times of crisis.

5) Countercyclical buffer- The macro-prudential purpose of this buffer is to protect financial system from possible crisis following the periods of excess lending growth. The buffer is set in a range between 0%-2.5%. When the National Bank sees a rapid increase in loans volume, it is authorized to impose countercyclical buffer of 2.5% and thus to slow lending pace. In the face of negative shocks, the countercyclical buffer should help the financial system not sharply curtail lending to the economy and thus further deteriorate the financial sector as a whole.

It is set on a quarterly basis and, if changed, by 0.25 percentage points or its multiplier. Countercyclical buffer is currently 0%.

6) Systemic buffer- is to increase systemically important financial institutions resilience, because financial difficulties arising in banks of systemic importance can pose a significant threat to the country's financial stability in a whole. JSC TBC Bank, JSC Banks of Georgia and Liberty Bank are considered as systemic banks in Georgia. Systemic risk buffer is up to 2.5% and will be fully imposed from 2021, currently only partial compliance is required.

Capital requirements under Pillar II:

7) Currency induced credit risk (non-hedged currency induced credit risk)- the aim of CICR buffer is to determine adequate capital buffer in order to reduce credit risk arising from exchange rate volatility. Balance sheet risk positions are considered non-hedged if they are denominated in a currency other than the currency of source of income. Such portfolio (foreign currency denominated, non-hedged loans) is subject to an additional 75% weighting and requires appropriate capital buffers. The amount of buffer depends on credit portfolio dollarization level of a particular bank.

8) Credit portfolio concentration risk buffer - consists of single name concentration buffer[1] and sectoral concentration buffer. Buffer requirement varies and depends on portfolio diversification level of particular banks in terms of groups and sectors.

9) Stress test buffer- The purpose of the stress-test buffer is to determine the amount of additional capital that, in the event of risk materialization against different scenarios in the course of supervisory stress tests, provides protection against bank default despite possible loss realization. The aforementioned stress test buffer will be effective in, 2020 (however exact time is not determined yet depending on stress test date itself) and will depend on the specific bank stress test results, which in turn will depend on the quality of the credit portfolio (customer payment capacity under certain stress scenarios). The amount of credit stress test buffer is calculated by

the following Basel formula:

10) GRAPE buffer- buffer set by national bank to a particular bank based on its general risk assessment and internal capital adequacy assessment programs. During determining named buffer, the inherent risks and their respective mitigations are taken into account. In the course of examination, internal capital adequacy assessment process, its quality, results and potential/planes are being challenged. Buffer requirement varies between banks according to different assessment results (on average 2.8%).

In the example of Georgia, Pillar II average requirement is 6.3% of total regulatory capital. Total minimum requirement (Pillar I+ Combined buffer + Pillar II) is up to 17% and fact up to 20% please, find the table 1 below:

Capital adequacy requirements for banks in Georgia:

Table 1

|

Q2 2019 |

Pillar II |

Total |

Fact |

||||||

|

|

CET1 |

Tier1 |

TC |

CET1 |

Tier1 |

TC |

CET1 |

Tier1 |

TC |

|

Ave. |

1.8% |

2.4% |

6.3% |

9% |

11.1% |

17% |

14.6% |

15% |

20% |

|

Min. |

0.7% |

0.9% |

2.7% |

7.7% |

9.4% |

13.2% |

11% |

11.7% |

16% |

|

Max. |

2.5% |

3.3% |

9.3% |

9.8% |

11.9% |

19.8% |

25.7% |

25.7% |

3% |

Author’s calculation. Retrieved fromhttps://www.nbg.gov.ge/index.php?m=109

Leverage ratio-The purpose of the ratio is to avoid the accumulation of excess leverage (the share of liabilities in the company's total capital) in the banking sector. The Leverage Ratio is a simple indicator that is a modern and effective complement to the Basel III Capital Adequacy Requirements (described above). Leverage ratio is calculated by dividing Tier1 Capital on risk position (on balance+ off balance) amount. The minimum requirement is set at 5% and is mandatory for all banks to comply from, September 2018.

Liquidity Coverage Ratio (LCR)- LCR is one of the most effective short-term (up to 30 days) liquidity-controlling indicator used internationally. LCR is calculated by dividing "high quality liquid assets" on "total net outflow" where "total net outflow" is the difference between the "cash outflow" and "cash inflow" within a 30-day period during stress event. High dollarization is also taken into account as additional threat during stress since, contingency plans or other mitigation tools by National Bank of Georgia are limited. The minimum level requirement for LCR in hard currency and separately on local currency are set at 100% and GEL 75% respectively. Requirement of 100% is mandatory for commercial banks from, September 1, 2017.

Net stable funding- The purpose of the ratio is to support the financing structure of commercialbanks' assets and off-balance sheet transactions. A stable finding structure reduces the risk of commercial bank solvency. The Net Stable Funding Ratio limits the dependence on short-term financing and stimulates a better assessment of the financing risk. Net Stable Funding Ratio is defined as Available Stable Funding divided on Required Stable Financing which must be at least 100%. Requirement is mandatory for commercial banks from, March 31, 2019.

Payment to income and Loan to value ratios- These are macro-prudential policy instruments that apply to loan terms. Loan servicing and collateral ratios affect the demand side and ensures the sustainability of both borrowers and banks.

PTI sets the maximum limit on costs related to loan which is determined by proportion of the borrower's disposable income. Find maximum possible defined limits in Table 2:

Table 2

|

Net Revenue (monthly) |

Non-Hedged Borrower Max./Contractual validity |

Hedged Borrower Max./Contractual validity |

|

<1,000 |

20% / 25% |

25% / 35% |

|

>=1,000-2,000< |

35% / 45% |

|

|

>=2,000-4,000< |

25% / 30% |

45% / 55% |

|

>=4,000 |

30% / 35% |

50% / 60% |

LTV determines the maximum loan amount according to the market value of the real estate that the loan is secured. This instrument, in the event of a fall in real estate prices, ensures the sustainability of the financial sector and also limits the emergence of a price bubble in the real estate market. Find, Table 3:

|

For loans in local currency |

85% |

|

For loans in foreign currency |

70% |

The requirement for these ratios has been effective since, November 2017. The ratios are subject to periodic adjustment by the National Bank of Georgia. The ratios that are provided in the table are currently effective and apply to all loans disbursed after 01.01.2019.

50% cap on effective interest rate of borrowings:

On 21.07.2018, amendment was made to 625 clause of Civil Law of Georgia, where maximum of 50% was introduced for all borrowings.

Regulation on lending standards on private individuals:

The provision on lending to individuals came into force on January 1, 2019. The requirements of the new regulation apply to all types of loans disbursed by a lending organizations or private individuals (including an individual entrepreneur). Under this regulation, all lending organizations are required to conduct a detailed client analysis, verify the source of income, and disburse loans within the established loan service and loan collateral ratios (described above).

The aim of the new regulation is to ensure the stable and sustainable functioning of the Georgian financial system and to encourage healthy lending ecosystem.

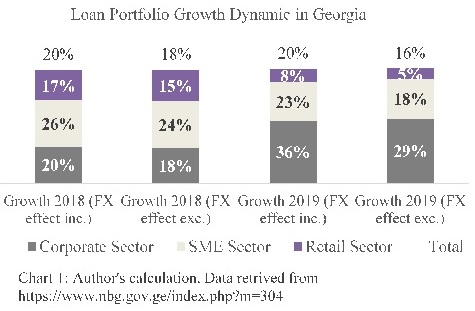

The effect of this regulation is clearly vivid by looking at the dynamics of the loan portfolio of retail sector during 12 months in 2019 and comparing it to the same period of 2018. In 12 months of 2019, the retail loan portfolio has increased by 8%, however if we exclude fx effect (local currency depreciated towards US dollar by 7%) retail portfolio growth was only 5%. If we compare it with the development of 12 months of 2018, when retail loan portfolio increase was 20% (18% fx effect excl.). Find, Chart 1:

5.Conclusion:

For the central banks this is indeed a challenge, as it is a very important trade-off in terms of reputation not to neglect financial stability on the one hand and not to lose credibility to the main objective of monetary policy on the other. Despite critical expert opinions, most central banks today agree that financial sector stability is and should be part of the monetary policy framework. However, price stability alone does not guarantee a stable financial system without adequate regulations and strict supervisory policies must also be in place. When monetary policy and banking supervision are brought under one roof, risks related to potential conflicts of interest, reputational risks and central bank independence should be mitigated. As it can be evidenced by the practices and tools described in this paper, the National Bank of Georgia successfully implements financial stability-oriented monetary policy.

References

- Financial Institutions- National Bank of Georgia (M3.1) retrieved from https://www.nbg.gov.ge/index.php?m=304

- Monetary Policy Operations Manual, National Bank of Georgia retrieved from https://www.nbg.gov.ge/index.php?m=720

- Marshal, F. (1998). Financial Engineering, Moscow М.:INFR–M,1998;

- Mankiw, G.N. and Taylor, M.P. (2007). Macroeconomics. Basingstoke: Palgrave Macmillan.

- Collard, F. Dallas, H., Diba, B. & Loisel, O. (2017). Optimal Monetary and Prudential Policies. American Economic Journal: Macroeconomics, 9 (1) (pp 40-87)

- Paoli, B. & Paustian, M. (2017). Coordinating Monetary and Macroprudential. Federal Reserve Bank of New York

- William G. Tierney & Randall F. Clemens (2011) Qualitative Research and Public Policy: The Challenges of Relevance and Trustworthiness. Center for Higher Education Policy Analysis University of Southern California.

- Rubio, M. & Carrasco-Gallego, J. (2016). Coordinating Macroprudential Policies within the Euro Area. University of Nottingham and University of Portsmouth. EconPapers: Economic Modelling, 59 (c) (pp 570-582)

- Svensson, L. E. (2017) The Relation between Monetary Policy and Financial-Stability Policy. Stockholm School of Economics, CEPR, and NBER.

- Rose, P. S., & Hundgins, S. C. (2005). Bank Management & Financial Services (7 ed.). McGraw-Hill/Irwin.

- Mishkin, F.S (1999). Lessons from the International Experience. Princeton, NJ: Princeton University Press.

- Mishkin, F.S (2004).Can Inflation Targeting Work in Emerging Market Countries? Graduate School of Business, Columbia University, and National Bureau of Economic Research

- Bank for International Settlements (2011). Basel III: A global regulatory framework for more resilient banks and banking systems.

- Regulation on Capital Adequacy Requirements for Commercial Banks (2018). Decree of the Governor of the National Bank of Georgia;

- Regulation On Credit Concentration and Large Risks in Commercial Banks (2019). Decree of the Governor of the National Bank of Georgia

- Regulation on lending standards on private individuals (2018). Decree of the Governor of the National Bank of Georgia

- Macroprudential Policy Strategy (2019), National Bank of Georgia retrieved from https://www.nbg.gov.ge/index.php?m=720

- Renewal of the Inflation-Control Target (2016). Bank of Canada retrieved from https://www.bankofcanada.ca/core-functions/monetary-policy/

- Financial Soundness Indicators-National Bank of Georgia (FSI) retrieved from https://www.nbg.gov.ge/index.php?m=304

- Act to Amend Civil Law of Georgia (2018) Clause 625

- Loans by Institutional Sectors-National Bank of Georgia (statistics) retrieved from https://www.nbg.gov.ge/index.php?m=10

[1] Single name concentration buffer: aims to determine adequate capital buffer on

concentration of top100 borrower’s exposure in credit portfolio.